Billing Basics

Premiums are collected between the 3rd and 5th business day of the month.

Account Types

| Checking / Share Draft | CHK, S/DR, ECHK, ES/DR |

| Savings / Share | SAV, SHAR, ESAV, ESHAR |

| Credit Card | CCRD, ECRD |

| Paper Bill | DBIL |

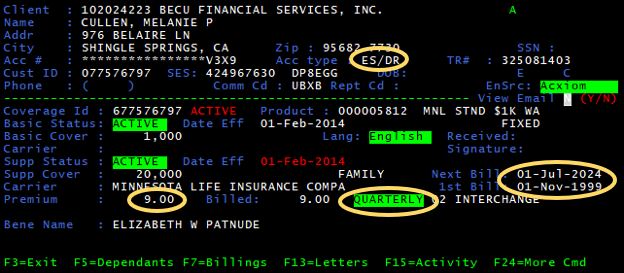

Quarterly Next Bill Date

FIRST CALL RESOLUTION TIP: It’s good practice to share the billing cycle with the customer

| Cycle 1 | Cycle 2 | Cycle 3 |

| January April July October |

February May August November |

March June September December |

Frequently Asked Questions

When is my next payment due?

“Your next payment is due (Next Bill).”

How much is my bill?

“You pay (Premium) (Billed).”

Which account is being debited?

“Your (Acc Type) account.”

When was I first billed for this insurance?

“Your first bill was on (1st Bill).”

How often am I billed?

“You are billed (Billed).”

How long have I had this coverage?

“You have had this coverage since (Date Eff).”

For AD&D, the effective date of the complimentary coverage could be different than the supplemental coverage.

Process Description

| Billing Types | Automated Clearinghouse (ACH)

Automated Clearing House (ACH) billing refers to the process where a financial institution distributes electronic debit/credit entries to bank accounts. With ACH transactions, financial institutions exchange checks and drafts drawn upon each other and settle daily balances. Debit/credit entries for premiums appear on the customer’s account statement. Credit Card (CCRD) Credit Card billing refers to the process where a credit company (Visa or MasterCard) charges premiums to the cardholder’s account. Charges for premiums appear on the customer’s account statement. Mortgage (MORT) Mortgage billing refers to the process where a mortgage company includes the premiums due in the homeowner’s monthly mortgage payment. The mortgage company bills the homeowner, reconciles the account and remits payment to Franklin Madison. CALL CENTER TIP: As premium is included in the insured’s mortgage payment and remitted to us by the mortgage company, representatives should not confirm the coverage status. Advise the insured that coverage is contingent upon continuous payment of premium remitted to Franklin Madison via the mortgage company. Because the mortgage billing process combines mortgage and premium payments, special circumstances can occur where the insured has over/under-paid premiums. This is typically due to timing of processing changes in coverage/premium amounts. Full premium not collected for 4 consecutive periods – coverage will be cancelled and a letter advising the insured that coverage is cancelled, with the option to restart their coverage Premium over paid – The insured will be issued a refund of the over-payment. The mortgage company will be notified of the correct premium that should be submitted. It is also important to understand that because premium is included on the insured’s mortgage payment, premium remittance is typically applied to the coverage one month in arrears. Ex. October premium would be received and applied with the client’s November remittance file. |

| First Billing | A customer’s first bill date is determined by the solicitation and the effective date. If Franklin Madison is unable to collect funds (premiums) for the first billing, coverage is automatically canceled. |

| General Billing Information | Each month, Franklin Madison bills its customers for millions of premium dollars and has several different billing arrangements with clients. While the Billing team is working to drive consistency, it is important to understand that billing procedure exceptions due exist.

The majority of our insured’s accounts are billed/charged for their premiums on or around the 3rdbusiness day of the month, according to their billing cycle. The remaining accounts are billed/charged sometime throughout the month, also depending on billing cycle. Once Franklin Madison extracts a billing file, it is forwarded to a Billing Processor. The Billing Processor is a third-party company, contracted to facilitate billing. The Billing Processor passes the billing file to the financial institution so that the accounts can be billed. Once the billing has posted, the Billing Processor sends the file back to Franklin Madison. A list of Billing Rejects is sent Franklin Madison from the financial institution after each billing, and are typically received within 5 to 6 days of the Posting Date.. Once the billing rejects are received, the Billing Department attempts to resolve as many of the rejects as possible, to prevent them from rejecting again. Later in the month, the accounts are coded for re-billing. It is important to note that there is no common naming for reject codes among financial institutions. What may be considered one reject reason at one financial institution may be considered a different reject reason at another. |

| Manual (Direct) | Manual or direct billing occurs when a physical bill is sent directly to the customer. There are very few cases where this occurs, and therefore considered an exception. |

| Premium Due Notice (PDN) | For all products (excluding Life Insurance products)…

If premiums are not collected after the re-bill, a Premium Due Notice is generated and mailed to the address on file. Franklin Madison will send three (3) notices in most cases*. The notices are referred to as PDN 1, PDN 2 and PDN 3 respectively. PDN information and history is listed as part of the coverage record. A Premium Due Notice is a courtesy reminder for the customer to remit premium in order to avoid a lapse in coverage. The PDN includes a tear-off portion and pre-addressed envelope for convenience. If the envelope is not available, advise the caller to send the PDN to: Franklin Madison Group If a customer wishes to send a PDN or payment overnight, advise the caller to send payment to: Franklin Madison Group |

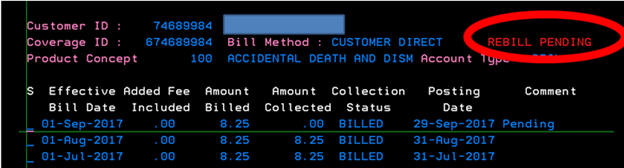

| Rebilling | If premiums are not collected as a result of a Soft Decline, Franklin Madison may repeat the billing process in an effort to collect funds. This is referred to as Re-Billing. A file is again sent to the Billing Processor, as for the regular billing, only later in the month – in an attempt to collect premium. When a coverage record has been soft declined and dispositioned to rebill, the “Rebill Pending” flash will be active within the coverage record’s billing history screen. This flash will remain activated until the rebill extract has been performed.

– Please note that not all financial institutions allow Re-billing. In those instances, a Soft Decline PDN is sent after receipt of the soft decline on the initial billing attempt, and the insured must remit payment manually through the PDN process in order to have payment applied to the billing effective period. |

| Tape (T-Code) | Tape or T-code billing occurs when a data tape containing billing information is physically mailed to the client. For this type of billing, there is little or no control over the post date. As a result, post dates for T-code billing are inconsistent. |

| Term Life Billing | All billing for the Life Insurance products occurs monthly, on or around the 5th business day. If premium is not collected due to a soft decline a Soft Decline letter will be sent to the insured and the premium will be re-billed later that month. If the premium is rejected as the result of a Hard Decline, a letter will be sent to the insured advising that they must provide an alternate billing account and the uncollected premium must be received by the 5th business day of the following month. The following months premium will be billed to the new account provided on our around the 12th day of that month. If the premium or new account information is not received by the due date, the coverage will terminate for non-payment and coverage cannot be restarted. |